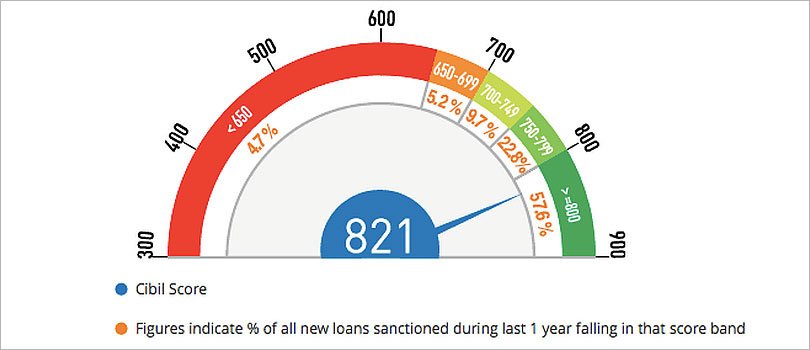

A person’s credit score plays a crucial role in determining his/her creditworthiness. In India, there are 4 credit bureaus licensed by RBI to provide credit scores. Amongst them, the most popular is CIBIL score and the words ‘CIBIL score’ are often used synonymously with ‘credit score’ and refers to a score ranging between 300 and 900, with 900 being the highest score possible.

The higher the score, the higher are the chances of an individual’s loan application getting approved. The credit score is important because it showcases how dependable or risky an individual is as a borrower.

This credit score is derived using the credit history found in CIBIL Report, also known as CIR i.e. Credit Information Report. It can be received by applying on the official website of CIBIL. Upon receiving it, understanding the CIBIL report becomes important to verify the accuracy of the information in the report.

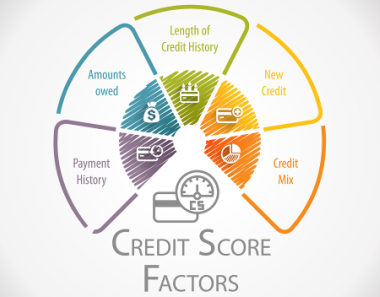

As an individual’s financial profile changes, so does his/her score. Therefore, knowing the factors affecting credit score is important as it gives an opportunity to an individual to improve his score over a period of time. Some of these are:

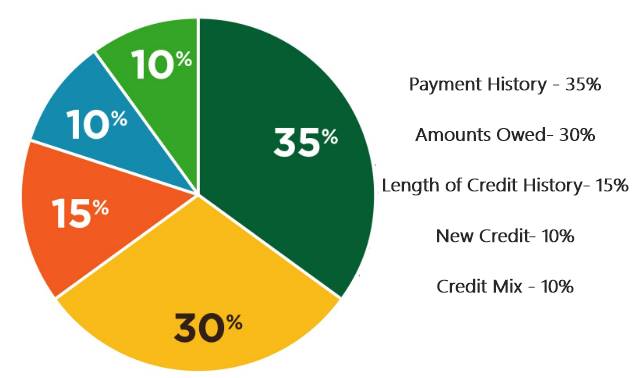

- Payment History– contributes to 35% of the total score

How timely you pay your bills affects your credit score most than any other factor. It implies that whether you can be trusted to repay the funds loaned to you or not.

- Credit Utilization– accounts for 30% of score

As a guideline, one should not use more than 30% of the available credit limit because it is a negative sign for creditors. Having too much debt or high balances can heavily affect one’s credit score.

- Credit History Length– makes up 15% of score

This includes both, the age of your oldest credit account and an average age of all your accounts. The longer your credit history, the higher your credit scores because it shows you have a lot of experience handling credit.

- Credit Mix– accounts for 10% of score

The more diversified portfolio of credit accounts a person holds such as installment loans, credit cards, mortgages, etc., the better it is for his credit score.

- New Credit– constitutes 10% of your credit score

The number of credit accounts you’ve recently opened as well as the number of hard inquiries lenders make when you apply for credit is another factor affecting the credit score. Too many inquiries, especially within a short span of time can affect your credit score adversely.

An individual with a credit score below 600 is generally considered to be a relatively high credit risk for a lender. Lending institutions often charge a higher interest rate on these individual’s mortgages than a conventional mortgage in order to compensate themselves for carrying more risk.

The Credit score of less than 750, calls for the need for credit repair services to help individuals improve their credit score and undo the damage done to their credit health because of faulty financial behavior in the past. Simply put, credit repair is the process of fixing your credit report due to the presence of some mistakes or inaccurate information. It becomes essential to rectify them as these errors can limit your access to different types of credit.

A credit repair company can be a great help to you during the credit repair process as it has the necessary experience and resources needed to get the job done right.

Conversely, a credit score of 750 or above is considered good and may result in the borrower becoming eligible for some best loan offers along with a lower interest rate on loans. Some of the actionable steps to increase the CIBIL score from 600 to 750 can be:

- First and foremost, an individual must ensure that there is no outstanding balance on his credit card.

- Secondly, one must manage his credit utilization in an efficient manner i.e. if you are using too many cards, you must close your idle cards and limit your credit usage. In contrast to this, if you own limited cards and are exhausting the limit every month, it is time to raise your credit limit by applying for a new card and thereby, reducing the credit utilization ratio.

- Repaying your loans on time will establish a good credit history of yours and will help you become eligible for a loan.

- Too many unsecured loans and credit card results in a low credit score. Therefore, one should try to balance the portfolio by applying for a secured loan as it is better for a profile.

- Instead of settling the loan, one must always refinance and close the account as this settled account is highlighted in the report as well.

- Consolidating too many loans and opting for a smaller EMI will help in boosting your score.

None of the above-mentioned points can guarantee instant results, but following some of these steps can definitely help in improving the score gradually. Rebuilding your credit health is not an impossible task. All that is needed is a certain amount of commitment and perseverance to achieve your credit goal.

Alternatively, you can meet the experts of the Credit Triangle to improve your credit score.